Since Friedrich Merz arrived at the chancellery, it seemed that Germany’s extreme and chronic aversion to debt was softening. First, in 2025, with the historic change in the Constitution relaxing the debt prohibition pushed by the current chancellor before he had even taken office; and later with the announcement of the huge investment of 780 billion euros in defense over five years. However, it now appears that either the transformation is not so radical or it only applies at home and not in the European Union, where the German “Nein,” so repeated during the financial crisis, is back.

Read more Lluïsa Moret: “More resources must be dedicated to municipal financing”

This is the signal Berlin has been sending in negotiations on the European budget, specifically the multiannual financial framework for the period 2028-2034, in which the old clashes between the frugal countries, the rich who consider themselves apostles of austerity, and the friends of cohesion, those who demand a push to bring their wealth level closer to the EU average, have been reborn. It also coincides with the German attitude towards proposals to use European debt to finance investments both in defense, the last-minute priority since we discovered that in this area we are alone; and in improving competitiveness, a deficit that has been dragging on for longer.

In this area, Merz makes it clear that Europe has to manage with the money available, a clear indication that cuts must be made in cohesion and agriculture spending, which take up about 60% of the budget. A recurring battle returns in Brussels.

Furthermore, the chancellor took the opportunity to repeat this at a very special moment, at the awarding of the Charlemagne Prize to Mario Draghi on May 14. “Super Mario” he called the famous Italian, highlighting his training and work ethic, inspired, he said, by the Jesuit Ignatius of Loyola. Merz praises the great Draghi, the author of the celebrated report which, after receiving all kinds of congratulations and laudatory adjectives, still has not been truly implemented.

It was even more curious when he placed his mentor, and former German Finance Minister, Wolfgang Schäuble, as the savior of the euro, on the same level as Draghi. “He was also a savior of the euro by systematically emphasizing the connection between monetary stabilization and reforms in the eurozone countries,” were his words.

Putting the man famous for the phrase “we will do whatever it takes… and believe me, it will be enough” on the same pedestal as the person who symbolized austerity at all costs during the financial crisis and who proposed a Grexit that almost happened, is an acrobatic exercise. It makes more sense considering who said it, a Merz who was Schäuble’s protégé and who shares much of his political legacy.

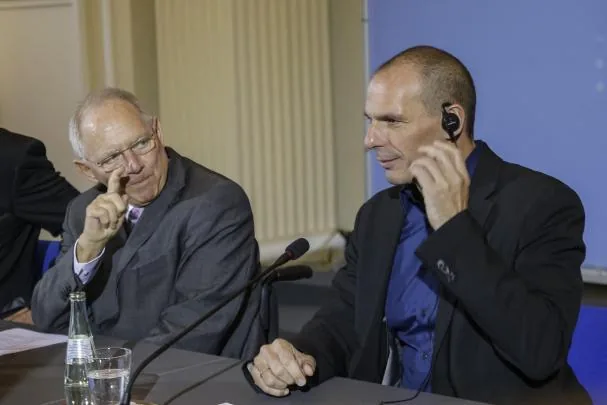

It was that Schäuble who starred in spectacular duels in Brussels with his Greek counterpart, Yanis Varoufakis. They only had the position in common, while ideologically they represented extremes and, regarding their personalities, contrasted the image of the serious and restrained German politician with the radical, exuberant, and provocative Greek. It is clear who won. It is true that Greece did not leave the euro, but the Greeks paid a high price; and while one marked European austerity policy, the other was a brief exuberant flower. He did not last even six months in office; with great prominence, but six months.

The Schäuble praised by the German chancellor starred in spectacular confrontations with the Greek Varoufakis

At the time, Schäuble was the target at which the Greeks threw their darts of frustration for the penance they had to pay, but in Germany they saw him differently. And they still do. Now, Merz has vindicated him by stating that “he contributed to saving the euro by tirelessly insisting on the relationship between monetary stabilization and reforms in the eurozone countries.” Many can confirm the tirelessly part.

Finished the flashback, let’s return to the present, because the German chancellor made very clear in Aachen his opposition to a possible common European debt, which slipped in among the praises to Super Mario. Merz acknowledges that more resources are needed but warns that excessive debt threatens sovereignty and limits the capacity to act. “Allow me to be frank: some countries already spend more on interest than on defense due to their colossal debt. We must not allow the European budget to reach that point.” That is, Germany combines massive investment in defense with a brake on European debt and, therefore, also a brake on one of the key points of the Draghi plan.

Also read

On the one hand, no more European sovereign debt, meaning that the recovery plan formula, however effective it has proven, served for one case, to respond to the effects of covid, but not to repeat it. The option of eurobonds, even if they are thought of not as they are usually identified, as a formula to help countries with problems, but to finance indispensable investments, does not have German support. The “Nein” returns, the frugals return. This time, without out-of-place comments about spending on drinks and women in southern countries, as a very frugal Dutch politician did in 2017. This time, very polite, but pointing to the same inflexibility.

Germany does not want European debt to finance investments

Moreover, on the other hand, it also represents a clear stance on the European budget, which they want to increase little, but especially change the structure. “More than two-thirds of European funds are still allocated to redistribution and subsidies. We cannot face the challenges of the 21st century with a 20th-century budget. Therefore, a deep modernization is indispensable,” said Merz. Read: fewer resources for agriculture, less for cohesion, and that they be redirected to innovation and defense.

This time it is not just a new episode of the recurring war between frugals and friends of cohesion, but also a discussion about the future, if we want a European Union capable of indebting itself to face new challenges. At one extreme are the cohesion supporters, who do not want to lose their manna, and at the other, the frugals, who veto a collective debt process.

We mentioned in a previous newsletter that eurobonds are like the Godots of the European Union, who never came and many think they never will, although people keep waiting for them. We said the moment is opportune because Europe now needs more than ever a powerful sovereign debt instrument and that its structure could be based on the proposal of economists Ángel Uribe and Olivier Planchart (“Now is the time for eurobonds”). An apparently very opportune moment, but which may end like Beckett’s play, with an eternal wait for Godot.

Read more Abuses against the flotilla open a new rift between Europe and Israel